Part 2/3 – Unique Challenges, Regulation, and Governance

If you were reading Part 1 of this series, you already know the potential: 6 use cases generating 35-50% ROI in 4-8 months. The opportunities are real.

But here’s the uncomfortable truth: implementing Generative AI in LATAM isn’t the same as doing it in the United States or Europe.

In this Part 2, we analyze the 5 unique challenges of LATAM and the mechanism by which AI governance becomes the barrier to entry that competitors will take years to replicate.

5 Problems Nobody Mentions in Vendor Presentations

If you read Part 1, you already know the opportunities are real. Now the uncomfortable part: why so many projects die before delivering results.

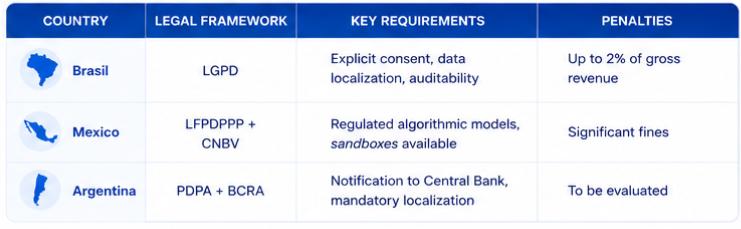

1. Three Countries, Three Regulatory Worlds

A bank operating in Brazil, Mexico, and Argentina doesn’t face “complex regulation.” It faces three systems that contradict each other.

The real problem: a solution designed for the US market and “adapted” for LATAM almost always violates something in some jurisdiction. Finding out after implementation costs ten times more than designing it right from the start.

2. Sophisticated Security in the Capital, Fragile 200km Away

Financial data is the greatest prize for any attacker. And LATAM has a distribution problem: first-class security infrastructure in São Paulo, Mexico City, Buenos Aires — but significantly weaker outside the capitals.

Cybersecurity talent is scarce and geographically concentrated. And Generative AI brought new attack vectors that many teams still don’t understand: prompt injection, data poisoning, model extraction.

The only viable answer is privacy by design: build protections into the architecture from day one, not patch them later.

3. The Chatbot That Works in São Paulo and Dies in the Interior

Mainstream AI platforms assume stable, high-speed connectivity. That works in capitals. In mid-sized cities and rural areas — where the greatest banking growth potential lies — it doesn’t.

A chatbot that needs constant calls to servers in Virginia works perfectly in a corporate office. It’s unusable for a customer in the interior of Brazil, Colombia, or Mexico.

If you want to expand financial services beyond major cities, you need solutions that work with limited bandwidth, unpredictable latency, and ability to operate partially offline.

4. The Talent That Doesn’t Exist

Data scientists who simultaneously understand Generative AI, Latin American financial regulation, and legacy banking systems practically don’t exist. And those who come close go work for Google, Microsoft, or relocate to markets that pay better.

This is the real reason so many projects stay in “permanent evaluation” phase: there’s no clarity about who will execute. The solution isn’t competing for impossible talent. It’s using platforms that can operate business users, not just data scientists.

5. The Model That Becomes Obsolete Before Implementation

In a stable economy, a credit scoring model trained 18 months ago still works. In Argentina, that model is garbage in 90 days.

Three-digit inflation. Devaluations. Drastic changes in how people spend, save, and pay. Traditional machine learning models, with 6-12 month retraining cycles, are structurally useless in this context.

Generative AI with automatic and continuous retraining isn’t a nice-to-have feature. It’s the minimum requirement to function.

Compliance: The Advantage Nobody Wants to Hear About

There’s a popular narrative in the tech world: regulation stifles innovation. In banking, that narrative is dangerous.

What Happens When You Ignore Compliance

- Regulatory fines and investigations (immediate risk)

- Every new AI expansion becomes more fragile (cumulative risk)

What Happens When You Take It Seriously

- Regulators know you and give you more room to innovate

- Customers trust you more — and in LATAM, where distrust in banks has historical roots, that’s a real differentiator

Compliance isn’t the opposite of innovation. It’s what makes it sustainable.

The 5 Pillars of Governance That Matter

You don’t need a 200-page framework. You need these five principles working:

1. Transparency

Any automated decision affecting a customer must be explicable. Not in technical terms, but in terms the customer and regulator understand. In Brazil and Mexico this is already an emerging requirement. In the rest of LATAM, it will be within 18-36 months.

2. Clear Accountability

Who is responsible if the model makes a mistake? If you can’t answer that question in 5 seconds, you have a governance problem. You need an AI Risk Officer with real authority, an approval process for each model, and documentation that isn’t cosmetic.

3. Fairness

Models trained on historical LATAM data learn its historical biases: unequal credit access by gender, discrimination by postal code, minority exclusion. Without active correction, AI doesn’t eliminate discrimination: it automates and scales it.

4. Privacy by Design

Not as an add-on. From day one: data minimization, localization by country, explicit consent, right to be forgotten.

5. Proactive Security

Generative AI brings new attack vectors. AI-specific penetesting, guardrails against prompt injection, incident plans for model failures. It’s not paranoia: it’s standard risk management in 2025.

N5’s Predictions for AI in LATAM Banks

At N5 we work with financial institutions across Latin America. We observe adoption patterns, talk with CTOs and CEOs, and see what’s working — and what isn’t — in real implementations. From that perspective, we make three predictions about how artificial intelligence evolves in regional banks.

Prediction 1: 40% of Customer Service Will Be AI by End of 2026

Today it’s at 15-20% in the most advanced banks. The economics are brutal: a human agent costing USD 8-12/hour competes against AI at fractions of a cent. The remaining 60% will stay human (complex cases, emotional sensitivity, customer preference). But the 40% that’s automatable will be automated.

Prediction 2: At Least 3 Mid-Sized Banks Will Be Acquired for Failing to Modernize

The pattern is known in Europe and the US: whoever doesn’t modernize sees their efficiency ratio deteriorate. Their competitors operate at 30-40% lower costs. The gap widens. A strategic buyer appears. In LATAM this will happen with 3-5 years of delay. The cost of modernization is still manageable today. In 18-24 months, it won’t be.

Prediction 3: AI Compliance Will Be the Biggest Competitive Differentiator by 2027

Institutions with robust governance will operate frictionlessly when new regulations arrive. Those without will have to build under pressure, on tight timelines, facing fines. Investment funds are already including “AI governance maturity” as an ESG criterion. It’s not just regulatory obligation: it’s a market asset.

What’s Next?

You know the challenges and understand why compliance matters. But the practical question is: is my bank ready? Where do I start?

In Part 3 we give concrete answers: a 5-dimension assessment to measure your maturity, a 4-step framework to start in weeks, and the 8 questions everyone asks (with direct answers).