Part 1/3 – Current State, Use Cases, and ROI

Five years ago, artificial intelligence in banks was a laboratory experiment. A team of data scientists in a basement, modest budgets, isolated use cases. CEOs approved pilot projects with moderate skepticism. CTOs promised results in 18 months.

Today, the conversation has changed completely.

Artificial intelligence — and specifically Generative AI — has stopped being an innovation project to become a strategic imperative. The banks leading the Latin American market in 2025 aren’t necessarily the largest ones. They’re the ones who made concrete implementation decisions in the last 24 months.

And those who didn’t are feeling the consequences.

In this 3-part series, we analyze the real state of artificial intelligence in regional banks: what’s working, what isn’t, what the specific challenges are, and how to start correctly.

The Current State of AI in LATAM Banks

The gap between perception and reality in the Latin American financial sector is notable.

What Executives Say:

- 71% of LATAM financial leaders consider Generative AI “critical” or “very important” to their strategy

- 81% planned to increase artificial intelligence investment in 2025

What the Numbers Reveal:

- Only 8% of large LATAM banks have advanced Generative AI implementations in production

- 58% of financial institutions in the region haven’t started any Generative AI project

- Only 19% have a clear, approved implementation plan

This gap isn’t corporate cynicism or lack of willpower. It’s the result of real challenges: complex regulation, unequal infrastructure, shortage of specialized talent, and legitimate uncertainty about how to implement correctly.

Latin America’s Position in Global Context

América Latina representa el 8 % del PBI mundial pero apenas el 3 % de la inversión global en inteligencia artificial.

La región invierte USD 2,8 billones anuales en IA — comparado con los USD 24 billones de Estados Unidos.

Latin America represents 8% of world GDP but only 3% of global artificial intelligence investment.

The region invests USD 2.8 billion annually in AI — compared to USD 24 billion in the United States.

At first glance, this seems like a significant disadvantage. But for leaders who know how to read the market, it’s exactly the opposite.

Financial institutions that move in 2025 won’t compete against mature, established solutions. They’ll define them.

In markets where 58% of the competition is still in “evaluation mode,” implementing Generative AI correctly today means 24-36 months of real competitive advantage before the market saturates.

The Market Country by Country

The reality of artificial intelligence in banks varies significantly by market:

Brazil: The Leader in AI Banking Adoption

Brazil leads the region in adoption. With over 1,200 active fintechs, the Brazilian financial ecosystem is the most dynamic in LATAM. The implementation of Open Finance and PIX — adopted by 140 million users — created a data infrastructure that facilitates AI implementations.

LGPD, while demanding, provides regulatory clarity that other jurisdictions still lack.

Mexico: Regulated Innovation

Mexico is the second market, with stable regulation and regulatory sandboxes that allow experimentation. The competitive pressure from fintechs like Mercado Pago and Nu Bank Mexico is accelerating the innovation agenda in traditional banks.

Argentina: Sophistication with Volatility

Argentina presents the most complex case: high financial sophistication combined with extreme macroeconomic volatility. AI models for credit risk must be capable of retraining monthly — a requirement that makes traditional solutions unviable.

Colombia and Chile: Progressive Regulators

Both countries have regulators that actively incentivize responsible innovation. They represent significant opportunities with moderate regulatory risk for well-designed implementations.

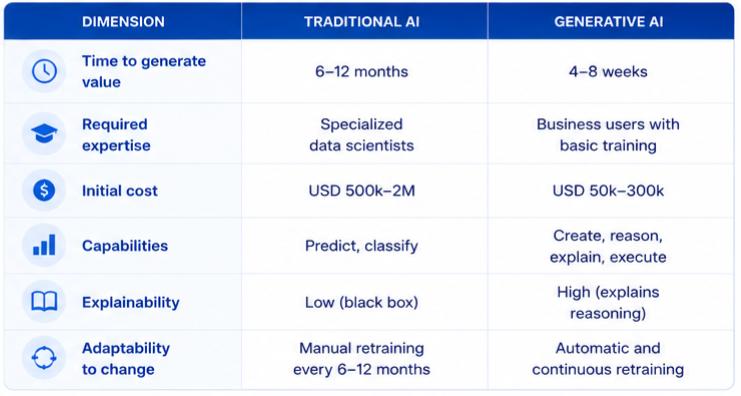

Generative AI vs. Traditional AI: The Difference That Defines Strategies

When technology leaders talk about “artificial intelligence in banks,” they frequently mix two fundamentally different categories. Understanding the distinction is critical for making correct strategic decisions.

Traditional AI: Predict and Classify

Traditional artificial intelligence — based on supervised machine learning — has been in the financial sector for over a decade. Its applications are well known:

- Credit scoring models that calculate probability of default

- Fraud detection systems based on transaction patterns

- Product recommendation algorithms

- Price and rate optimization

These systems work well within their limits. They’re specialized, predictable, and auditable. But they have clear restrictions: they require large volumes of labeled data, take months to implement, and can’t do anything they weren’t explicitly trained to do.

Generative AI: Create, Reason, and Act

Generative AI is a different category in almost every dimension that matters to a CTO:

Why This Difference Matters Strategically

For a mid-sized bank in Colombia without a data science team: traditional AI was inaccessible. Generative AI isn’t.

For a bank in Argentina where credit patterns change every quarter: traditional AI with semi-annual retraining is useless. Generative AI isn’t.

The question is no longer whether to adopt Generative AI. It’s when and how.

The 6 Use Cases with Highest ROI for Artificial Intelligence in Banks

Not every application of artificial intelligence in banks has the same value. These are the six use cases that consistently generate the greatest return for financial institutions in Latin America.

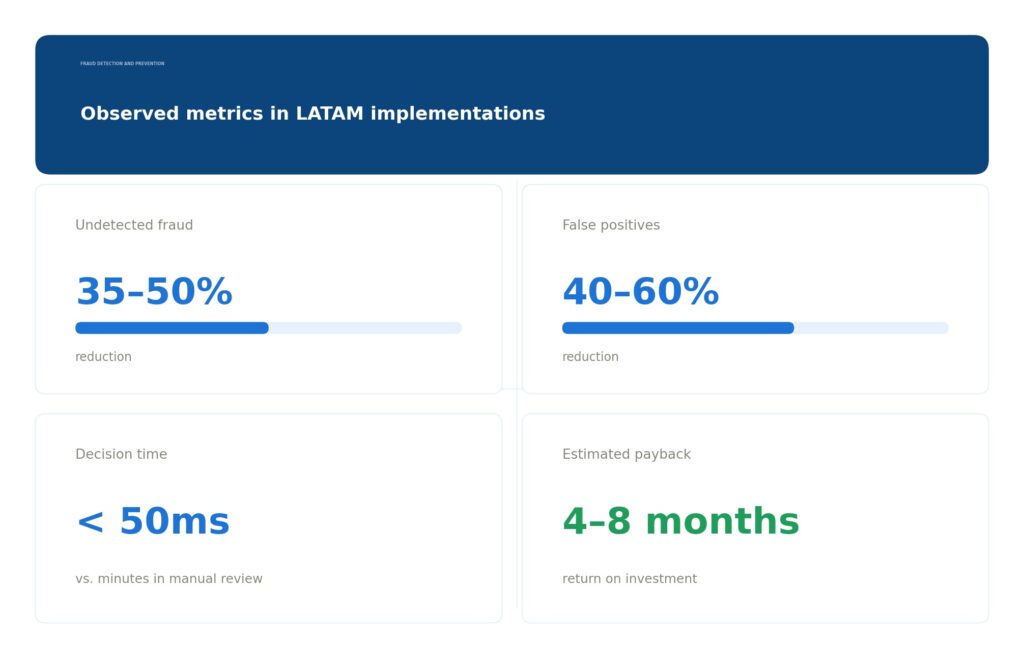

Use Case 1: Fraud Detection and Prevention

Latin America loses approximately USD 1.2 billion annually in financial fraud. Static rule-based detection systems capture 60-70% of actual fraud — and generate a volume of false positives that creates friction for legitimate customers.

How Artificial Intelligence Transforms It:

Generative AI models for fraud analyze behavior patterns in real time, not in batches. They can detect fraud techniques that weren’t anticipated in system design. And crucially, they can reduce false positives by 40-60% — meaning fewer legitimate customers blocked and fewer call center calls about disputed charges.

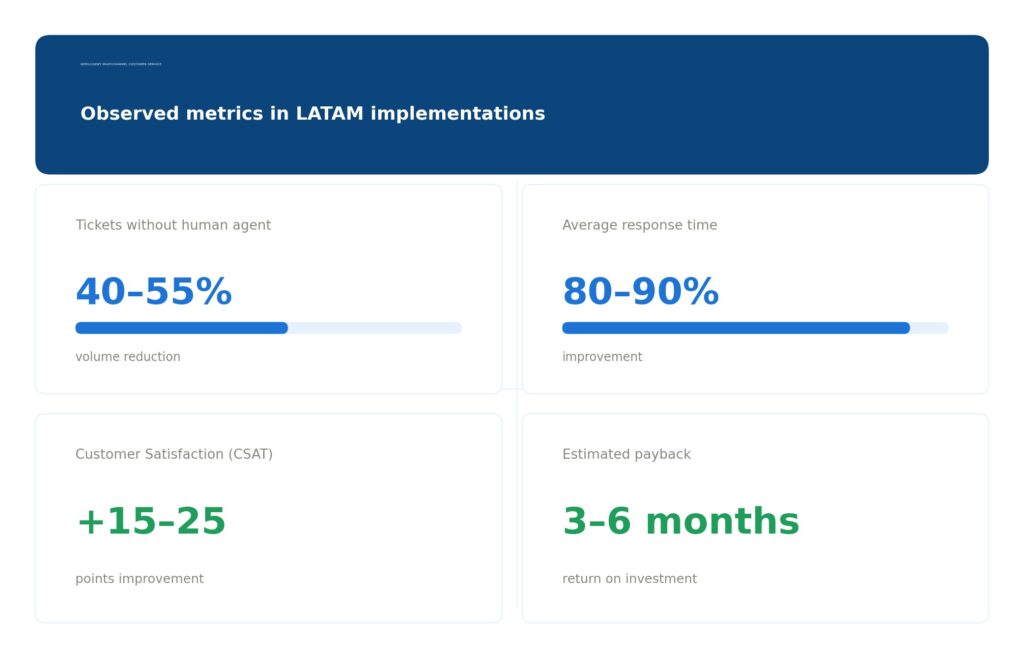

Use Case 2: Intelligent, Multi-Channel Customer Service

The contact center is the largest operational cost for most LATAM banks. One human agent costs USD 8-12 per hour. One Generative AI interaction costs fractions of a cent.

But more important than cost is quality. First-generation chatbots (based on decision trees) can only answer anticipated questions. Generative AI understands context, maintains conversation history, can execute transactions, and escalates complex cases to human agents with full context.

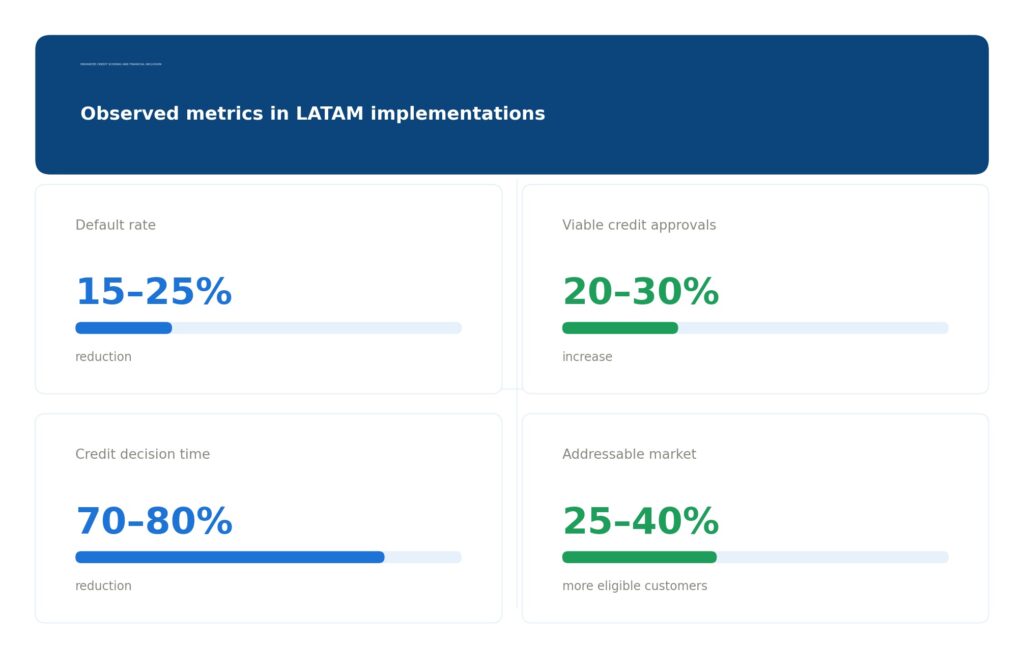

Use Case 3: Improved Credit Scoring and Financial Inclusion

50% of Latin America’s population is “unbanked” or “underbanked”. The problem isn’t lack of demand. It’s that traditional scoring models exclude those without formal credit history.

Generative AI can analyze alternative signals — behavior on ecommerce platforms, service payment history, mobile usage patterns — to build credit risk profiles for customers without banking history. With appropriate customer consent.

For markets with high macroeconomic volatility (Argentina, Venezuela), automatic model retraining is critical. A system that can’t adapt to 200% inflation is useless for assessing credit in that context.

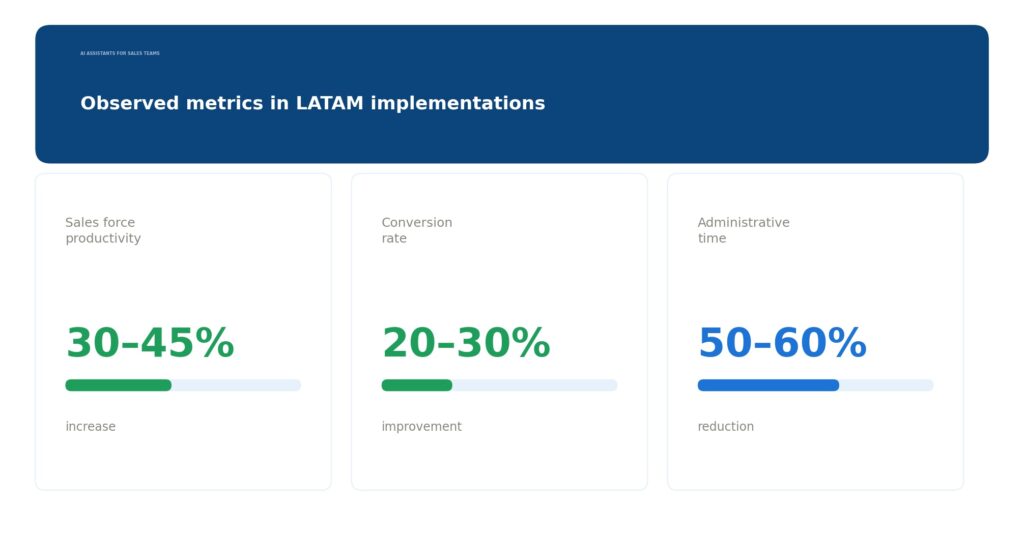

Use Case 4: AI Assistants for Sales Teams

Bank sales teams spend 40-60% of their time on administrative tasks: recording visits, updating CRM, preparing proposals, looking up customer information. Tasks that steal selling time.

Generative AI assistants — copilots that work alongside the executive, not replacing them — automate these tasks:

- Listen to a sales call and automatically generate summary and next steps

- Access complete customer history in seconds

- Suggest next best action based on customer context

- Draft personalized proposals in real time

The result for the bank: executives who can serve more customers with better quality, without increasing headcount.

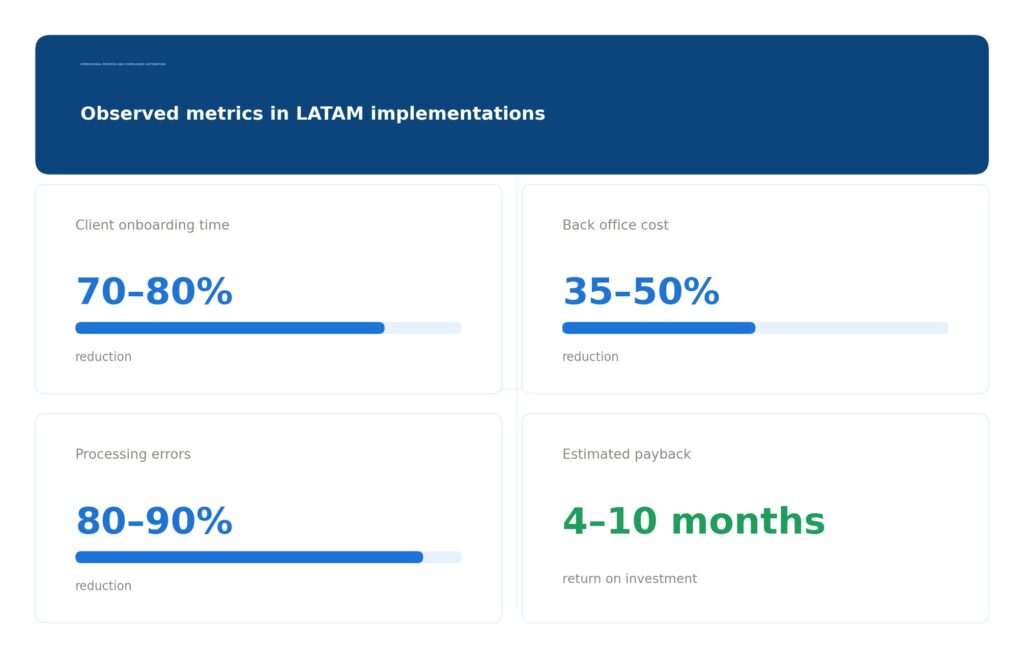

Use Case 5: Operational Process and Compliance Automation

The back office of LATAM banks is frequently the area with greatest improvement potential. Manual processes, legacy systems that don’t communicate with each other, manual document review, reconciliations that take days.

The combination of OCR (optical character recognition) with Generative AI enables:

- Process and extract information from documents in seconds

- Automate KYC (Know Your Customer) validations

- Generate regulatory reports automatically

- Detect data inconsistencies that previously required human review

For compliance specifically: AI can monitor transactions for money laundering signals, generate explanatory documentation for regulators, and maintain complete audit trails, reducing regulatory fine risk.

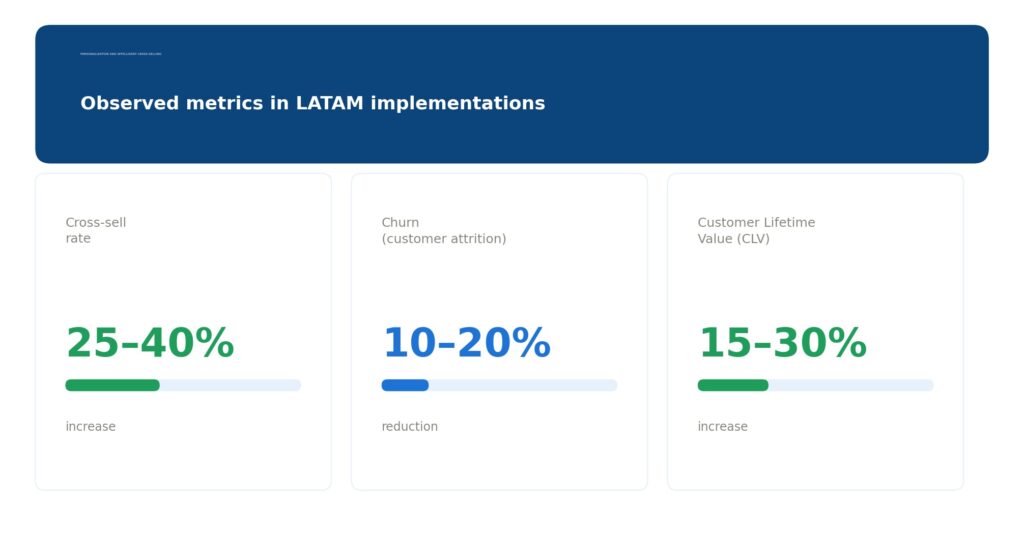

Use Case 6: Intelligent Personalization and Cross-Selling

Most bank customers in LATAM have 1-2 products with their primary institution. The cross-selling potential is enormous — but generic offers have minimal conversion rates.

Generative AI can analyze the customer’s complete behavior — transactions, interactions, detectable life events, comparisons with similar segments — and generate genuinely personalized recommendations, at the right moment, through the right channel.

What’s Next?

You know the landscape and the use cases. But implementing AI in LATAM isn’t copying what a bank did in Europe.

There are region-specific challenges that most underestimate — and that can paralyze an entire project if not anticipated. In Part 2 we discuss this: multi-jurisdictional regulation, unequal infrastructure, talent shortage, macroeconomic volatility, and why compliance isn’t a brake but an advantage.