Open Finance: Projections of Latin America | N5

Open Finance is a trend that is advancing by leaps and bounds around the world. Currently, Europe is one of the leading regions in its application, but the rest of the continents are not far behind.

On this occasion we will review the latest trends in open finance in Latin America, including how they affect the new generations and what is the status of different countries in the region on the scale of acceptance.

See more information about Open Finance

Open Finance in Latin America

Everything points to the Open Banking It will not stop growing in the coming years. According to data from the consulting firm PriceWaterhouse Coopers, it is expected that in 2022 the total income of this modality will reach 9,870 million dollars in the world — and South America is showing itself more and more favorable to this.

The Latin American scenario (low bank penetration, high penetration of mobile telephony and the Internet, and a mostly young population) is ideal for traditional players and new digital fintech companies to easily provide Open Finance services.

Según Belvo, el 84,8% de los profesionales fintech creen que cada vez más empresas adoptarán According to Belvo, 84.8% of fintech professionals believe that more and more companies will adopt open finance models in 2022. The majority of those surveyed indicated that credit services will be the fintech models that benefit most from Open Finance. Credit scoring and personal finance management tools followed.

In order to launch and implement open finance in Latin America, a large majority of fintech professionals believe that bank data is the alternative data source from which they will benefit the most to create new products. These are followed by the data that technology companies can provide thanks to Big Data.

As the numbers indicate, everything indicates that the market is preparing for a gigantic growth in the sector.

Millennials and Gen Z: Technology adapted for new generations

There is a taboo that assumes that the new generations are not so interested in finances. However, as everything indicates, this could not be further from the truth.

In Latin America, millennials and members of Generation Z are increasingly using their mobile phones to carry out payments or typical banking activities. This is putting pressure on banks to deliver the seamless, digital financial experiences these individuals expect..

Banks across Latin America need to keep a close eye on how the preferences of these younger consumers are changing, especially given the weight they are gaining on a massive scale..

Traditional financial institutions and emerging fintechs or other payments players looking to launch their services within the region need to ensure they are optimizing their offerings to reflect the needs of these generations.

These entities must find a way not only to differentiate themselves from emerging fintechs or neobanks that offer new products with digital priority in increasingly saturated markets such as Latin America, but also to offer services that are easily connected with other financial characteristics. so that they feel personalized to your own needs.

This customer profile no longer expects a single financial institution to meet all their needs for solutions and services, and with the advent of open banking. They want to have widely integrated experiences

Growing Interest in Super Apps

Both millennials and Gen Z consumers are expressing interest in so-called “super apps,” financial services that tie together multiple platforms or solutions with the help of technologies like application programming interfaces.

These types of connected apps are set to become more popular as these consumers exert more influence over the financial industry on a global scale..

An Ally for the Expansion of Open Finance

As millennial and Gen Z consumer expectations of their banking experiences begin to reimagine industry standards, offering hassle-free, personalized financial services is likely to become even more important for financial institutions in Latin America..

Therefore, open finance, which uses technologies such as APIs to connect banking services, is set to play a more dominant role in the future of the financial industry.

It’s critical for financial institutions to be vigilant about the potential benefits of open finance, as millennials and Gen Z demand faster and easier access to a growing list of emerging banking and payment functions..

Key Trends of Open Banking in Latin America

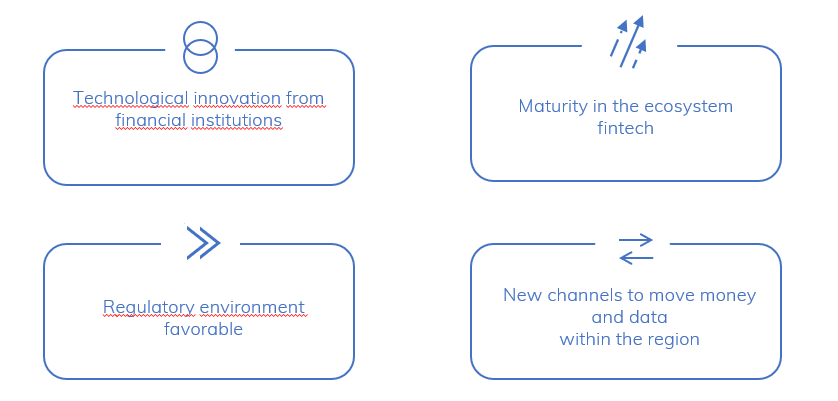

We can identify four key trends that are accelerating the expansion of Open Banking in Latin America.

- Technological innovation from financial institutions

- Maturity in the fintech ecosystem

- Favorable regulatory environment

- New channels to move money and data around the region

The Role of Technological Innovation

In recent times, alliances between traditional banks and fintechs have fostered innovation. Banks based in Latin America are increasingly partnering with fintech companies and launching API platforms to stay competitive.

As fintechs reach consumers that traditional banking cannot, they open up the ecosystem and create opportunities for collaboration. APIs allow banks to reduce costs, increase efficiency, improve communication and reach new customer segments.

The incursion of foreign companies in the region also brings improvements in innovation. The growth potential in Latin America is also attracting European fintech companies, which recently announced their expansion to the region.

In October 2021, UK-based fintech company Revolut announced plans to start operations in Mexico as its first step into the Latin American market. German digital bank N26 acquired a digital banking license for Brazil in 2021, after the pandemic delayed its plans to enter the market.

Maturity in the Fintech Ecosystem

The region’s fast-growing fintechs are also showing signs of maturity. Nubank has expanded beyond Brazil, to Mexico and Colombia.

In the third quarter of 2021, Nubank had 48.1 million customers, a huge increase from the 3.7 million customers in the first quarter of 2018.

Without a doubt, this is an example of the growth potential that these technologies have in Latin America.

New Channels to Move Money

The launch of real-time payment services such as PIX, Yape and PLIN is driving the growth of electronic payment volumes.

As fintechs launch affordable, low-cost trading platforms and financial education increases, while interest rates remain low, more consumers are turning from low-yielding savings accounts to new investment products.

Favorable Regulatory Environment

The unprecedented technological changes taking place in the region are putting pressure on regulators to act more quickly. Brazil, Mexico and Colombia are already working on their regulations for Open banking.

Regulatory development in Latin America in the coming months will continue to be largely driven by activities in Brazil, Colombia and Mexico, where regulators are expected to continue to introduce specific guidelines for full implementation of local frameworks before the end of 2022.

API platforms increased 147%, to 47 in Latin America, as participating banks in Brazil advance in implementing open finance and holders in Mexico start sharing information about products and services.

Fintech Trends in the Region

The Latin American region is in one of its fastest growing moments when it comes to digital finance technologies. These are the most predominant trends today:

QR Payment

In 2022 there are more options to make payments, one of the main ones, QR, mainly through entities such as Mercado Pago. This has made an alliance with the state bank and the Santiago metro network so that people can pay for their ticket through a QR.

Examples like this are expected to be seen during the rest of the year as people are increasingly looking for new easy, affordable and 100% digital forms of payment.

Adaptation to the digital world

It is estimated that by the end of 2022, Fintechs will no longer be the only ones within the digital financial ecosystem, as we have seen how traditional and government banking entities are beginning to migrate to digital with products, laws and services adapted to this new era.

This not only supposes a new competition towards Fintechs, but also a new way of involving financial inclusion in consumers.

Crypto Trend

Another trend to watch out for in 2022 is central bank digital currencies. These are digital versions of fiat currencies like the dollar and their ultimate goal will be to replace cash.

In Argentina, the penetration of this trend is bringing the best talents to the crypto ecosystem, we are seeing wallets like Belo, Buenbit, Lemon growing by leaps and bounds and eager to eat up the Latin American market. Likewise, we see DeFi protocol projects on the rise.

Buy Now Pay Later

BNPL is the new “pay in installments”. It works as a short-term financing, which generally does not charge interest if the client complies with their payments in a timely manner. BNPL is another trend in favor of financial inclusion in the region, and the possibility of more connected customers buying also benefits businesses.

There are good prospects in the region, especially due to the growth of electronic commerce and we see that companies within this model are raising large amounts of money in important investment rounds. Investors see giant potential in these companies, especially in Mexico. A Good Regulation

The issue of regulation is going to be a trend during 2022, with BigTech as protagonists, since it is estimated that the data will continue to be very relevant within the phases of the creation of an updated Fintech law adapted to the digital age.

5G breakthrough

More reliable and 100 times faster than current technology, this new interface will impact every industry and is expected to contribute $13.2 trillion to the global economy by 2035. Although the COVID-19 pandemic delayed the implementation of 5G, 1 billion subscriptions are expected worldwide this year.

How are the countries advancing?

Although Open Finance is gaining more and more strength, each country is at a different stage in terms of its adoption.

- Brazil: Brazil is a pioneer in digital adoption, and its open banking regulations place the country at the forefront of adoption worldwide. In fact, it is already in the final stages of its full acceptance. Phase 4 of open banking began in December 2021 and is expected to last until 2022. The last stage is marked by the start of open finance, and will include investment data, insurance, pensions and foreign exchange services.

- México: March 2018, Mexico published the Law to Regulate Financial Technology Institutions. This was one of the first global steps to regulate the Fintech sector and the open banking model. This law establishes that all financial institutions are required to share information. On March 10, 2020, the Bank of Mexico published the first open banking rules that focused mainly on public data

- Perú: Although Peru has not established any specific regulations for open finance, the country’s financial institutions have already been sharing customer data for some time. Recently, Bill No. 1584/2021-CR was presented, which declares the implementation of a public policy that encourages the mass use of open banking or also known as Open Banking to be of national interest and public necessity.

- Argentina: Hasta ahora, Argentina no tiene regulaciones oficiales sobre open banking. El Banco Central de Argentina ha promovido cierto diálogo en torno a iniciativas de open banking. El BCRA y la Unidad de Información Financiera han incorporado en sus reglamentos algunas disposiciones para fomentar el open banking, como permitir a los bancos compartir información de los clientes a petición de éstos. Si bien no existe un marco oficial, el Banco Industrial lanzó su plataforma Banco de APIs con Poincenot Technology Studio en 2018, convirtiéndose en el primer banco de Argentina en ofrecer APIs abiertas al mercado.

- Chile: Until now, Argentina has no official regulations on open banking. The Central Bank of Argentina has promoted some dialogue around open banking initiatives. The BCRA and the Financial Information Unit have included in their regulations some provisions to promote open banking, such as allowing banks to share customer information at their request. Although there is no official framework, Banco Industrial launched its Banco de APIs platform with Poincenot Technology Studio in 2018, becoming the first bank in Argentina to offer open APIs to the market.

- Colombia: Industry stakeholders held a summit in August 2021 hosted by the Open Banking Exchange to collaborate on the development of open finance. A decree outlining the structure for institutions overseeing the adoption of open finance is expected in 2022.

Conclusions on Open Finance Trends

Open Finance is about a current that gains more strength year after year. These are the main points to understand its evolution in Latin America:

- As you have had the opportunity to see, Open Finance is a trend that does not stop growing — little by little, more and more entities decide to adopt this model.

- The new generations are gaining more and more strength in the financial sector, precisely thanks to these new technologies.

- Technological innovation, maturity of the fintech model, and new types of payments, combined with a favorable regulatory environment, further promoting the expansion of the Open Banking trend

- There are a series of trends that you are currently leading in the region, including means of payment, new types of financing, and a more marked technological advance

- Brazil and Mexico continue to be leaders in the development and progress of Open Finance, but the rest of the countries are laying the foundations

For more information, please access our downloadable